Ever picked up your prescription and been shocked that your generic drug cost more than the brand-name version? You’re not alone. Many people assume generics are always the cheapest option - but that’s not true anymore. Thanks to how insurance plans are structured, some generic medications now sit in higher tiers with steeper copays. And the reason has nothing to do with how well the drug works.

How Tiered Copays Work

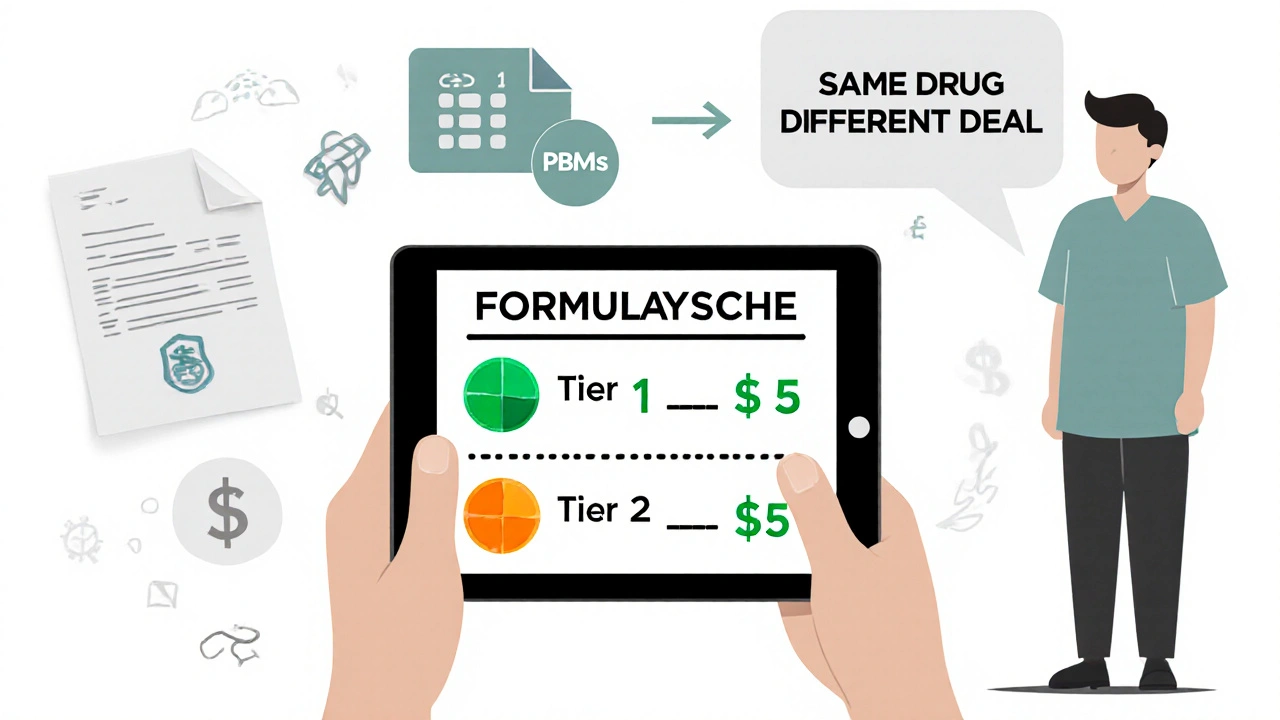

Most health plans today use a system called tiered copays. It’s like a pricing ladder for your prescriptions. The lower the tier, the less you pay. Tier 1 usually has the cheapest drugs - often preferred generics. Tier 2 might include other generics or preferred brand-name drugs. Tier 3 and above? That’s where things get expensive. Non-preferred brands, specialty drugs, and yes - some generics - can land there.Here’s how it breaks down in most plans:

- Tier 1: Preferred generics - $0 to $15 for a 30-day supply

- Tier 2: Non-preferred generics or preferred brand-name drugs - $20 to $50

- Tier 3: Non-preferred brand-name drugs - $60 to $100

- Tier 4: Preferred specialty drugs - 20% to 25% coinsurance

- Tier 5: Non-preferred specialty drugs - 30% to 40% coinsurance

But here’s the twist: not all generics are in Tier 1. About 12% to 18% of generic drugs are placed in Tier 4 or 5 because they’re complex, treat rare conditions, or cost more than $600 a month. Others? They’re bumped up to Tier 2 just because the manufacturer didn’t offer a big enough rebate to the pharmacy benefit manager (PBM).

Why Your Generic Isn’t Cheap - Even Though It’s the Same Drug

Let’s say you take levothyroxine for your thyroid. You’ve been paying $5 a month for years. Then one day, your copay jumps to $45. You call your pharmacy. They say it’s still the same drug. Your doctor says all generics are chemically identical. So what changed?The answer: the rebate deal expired.

Pharmacy Benefit Managers - companies like CVS Caremark, Express Scripts, and OptumRx - don’t pick tiers based on effectiveness. They pick them based on money. When a drugmaker agrees to give the PBM a big discount (called a rebate), the PBM puts that drug in Tier 1. If another generic version of the same drug doesn’t offer the same discount, it gets pushed to Tier 2 or 3 - even if it’s made by the same company, in the same factory, with the same ingredients.

A 2023 report from Avalere Health found that 68% of generic drugs moved to higher tiers were due to expired rebate contracts, not safety or efficacy concerns. That means your $45 generic isn’t better or worse - it’s just the one your insurer didn’t negotiate a deal with.

Who’s Behind the Scenes? The Role of PBMs

PBMs are the middlemen between drug manufacturers, insurers, and pharmacies. They negotiate prices, manage formularies, and decide which drugs go on which tier. They don’t work for you. They work for the insurance company - and their job is to reduce overall drug spending.That sounds good, right? But here’s the catch: the savings don’t always go to you. PBMs keep a portion of those rebates. And when they push a cheaper generic to a higher tier, they’re not trying to save you money - they’re trying to steer you toward the drug that gives them the biggest cut.

Dr. Aaron Kesselheim from Harvard Medical School put it bluntly: “Tiering generics differently undermines the fundamental purpose of generic substitution.” In other words, if you’re paying more for the same medicine, the system isn’t working the way it should.

Real Stories, Real Confusion

On Reddit, a user named PharmaPatient87 wrote: “My levothyroxine generic went from $5 to $45 overnight. My doctor says all generics are the same. Why won’t my insurer explain this?”You’ll find similar stories everywhere. A 2023 survey by the Patient Advocate Foundation found that 41% of insured adults had a generic drug suddenly cost more - and 68% couldn’t get a clear answer from their insurer.

Some patients get stuck with automatic substitutions. The pharmacist switches your $5 generic to a $45 one because that’s the one the plan prefers. You don’t know until you pay at the counter. And if you don’t speak up, you keep paying more.

One woman with rheumatoid arthritis was hit with a $3,200 monthly bill for a generic version of adalimumab. She thought it was a mistake. It wasn’t. Her plan classified it as a specialty drug - even though it was chemically identical to the $200 version her friend got.

What You Can Do

You can’t change the system - but you can work around it.- Check your formulary every year. Plans update their tiers on October 1. Don’t wait until your prescription runs out. Log in to your insurer’s website or call customer service and ask for the current formulary.

- Use tools like GoodRx or SmithRx. These sites show you what different versions of the same drug cost at nearby pharmacies - even if your insurance doesn’t cover them. Sometimes paying cash is cheaper than your copay.

- Ask your pharmacist to check for alternatives. Pharmacists know which generics are in which tier. Ask: “Is there another version of this drug that’s cheaper under my plan?”

- Request a therapeutic interchange form. If your doctor agrees, they can fill out a form asking your insurer to cover a different version. This works 63% of the time, according to the Medicare Rights Center.

- Look into manufacturer assistance programs. Many drugmakers offer discounts or free medication for low-income patients. Even for generics, these programs can cut your bill by 20% to 50%.

What’s Changing in 2025 and Beyond

The Inflation Reduction Act, starting in 2025, will cap out-of-pocket drug costs at $2,000 a year for Medicare Part D users. That’s huge. But it doesn’t eliminate tiered copays. It just limits how much you pay total.Some insurers are already simplifying. UnitedHealthcare moved popular generics like atorvastatin and lisinopril to $0 copays in Tier 1. But less common generics? They’re now $10 - still higher than before.

Experts predict tiered systems won’t disappear. But they’ll likely shrink from 5 tiers to 4 by 2026. The bigger issue? Biosimilars - generic versions of complex biologic drugs - are coming. And insurers will likely tier them too. That means even more confusion for patients with conditions like arthritis, diabetes, or cancer.

The Bottom Line

Your generic drug isn’t expensive because it’s less effective. It’s expensive because the system rewards rebate deals over patient savings. The same pill, same manufacturer, same results - but a different price tag based on a contract you never saw.Don’t assume your insurer has your best interest in mind. Stay informed. Ask questions. Push back. And if you’re paying more for the same medicine, you’re not being unreasonable - you’re just paying for a broken system.

Why is my generic drug more expensive than the brand-name version?

It’s not about the drug - it’s about the rebate. Insurance companies and pharmacy benefit managers (PBMs) negotiate deals with drugmakers. If a generic manufacturer doesn’t offer a big enough discount, their version gets placed in a higher tier with a higher copay - even if it’s chemically identical to a cheaper generic. The brand-name drug might be in a lower tier because its maker pays a bigger rebate.

Are all generic drugs the same?

Yes, legally. All generic drugs must meet the same FDA standards for active ingredients, strength, dosage, and safety as the brand-name version. The only differences are in inactive ingredients like fillers or coatings - which rarely affect how the drug works. But insurers can still charge different prices based on which manufacturer made it and what rebate deal they struck.

How do I find out what tier my drug is on?

Log in to your insurance plan’s website and look for the “formulary” or “drug list.” Most insurers update it every October. You can also call customer service and ask for the current formulary. Third-party tools like GoodRx or SmithRx let you compare copays across different versions of the same drug.

Can I switch to a cheaper generic without changing my prescription?

Sometimes. Pharmacists can substitute a preferred generic automatically - but only if your doctor hasn’t written “dispense as written” on the prescription. If you’re getting hit with a higher copay, ask your pharmacist: “Is there another version of this drug that’s cheaper under my plan?” If yes, they can often switch it without needing a new prescription.

What if my drug moved to a higher tier mid-year?

You can file an exception request. Ask your doctor to fill out a “therapeutic interchange” form explaining why you need the current drug. Many plans approve these requests if the alternative would be less effective or cause side effects. You have 72 hours to appeal if it’s urgent. Don’t wait - call your insurer as soon as you notice the price change.

Are there programs to help pay for expensive generics?

Yes. Many drug manufacturers offer patient assistance programs, even for generics. These can reduce your cost by 20% to 50%. Check the manufacturer’s website or call their customer service line. Nonprofits like the Patient Advocate Foundation and NeedyMeds also help people find free or low-cost medications.

Will the $2,000 out-of-pocket cap in 2025 fix this problem?

It helps, but it doesn’t fix the root issue. The cap limits how much you pay in total - but your insurer can still charge you more per prescription. You might hit the cap faster because each drug costs more. The tiered system stays in place. You’ll still be paying higher copays for the same drug - just not as often.

Written by Felix Greendale

View all posts by: Felix Greendale